Banks' Dangerous Dependence On The Fed

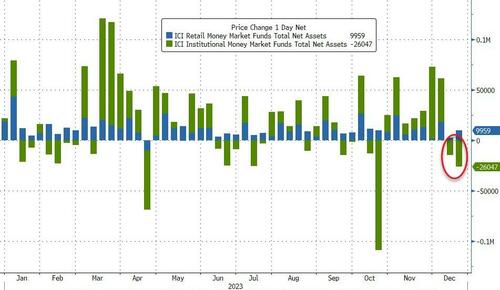

For the second week in a row, money-market funds saw outflows, down $16.1BN this week,

Source: ZeroHedge

Once again, institutional funds were responsible for all the outflows (-$26BN) while retail funds continued their streak on inflows (+$10BN) that is unbroken since April...

Source: ZeroHedge

In a breakdown for the week to Dec. 20, government funds - which invest primarily in securities like Treasury bills, repurchase agreements and agency debt - saw assets fall to $4.79 trillion, a $24 billion decline.

Prime funds, which tend to invest in higher-risk assets such as commercial paper, meanwhile, saw assets rise to $955 billion, a $7.66 billion increase.

“This is a turning point and you do start to see money move out of money markets, into riskier assets, into term rates to lock in higher rates,” Jeffrey Rosenberg, a portfolio manager at BlackRock Financial Management said in a Bloomberg Television interview.

“As cash rates start to come down, you’re penalized in 2024 for holding cash because the rates and the prospect of the rates is to go lower.”

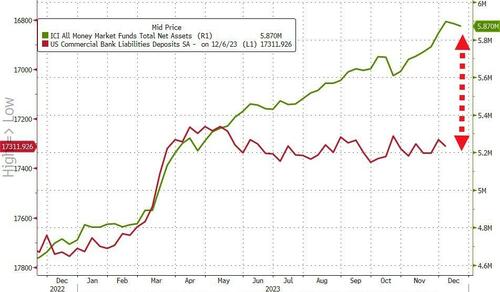

So, is this divergence starting to narrow?

Source: ZeroHedge

Notably, the exodus from The Fed's reverse repo facility has stalled in recent days

Source: ZeroHedge

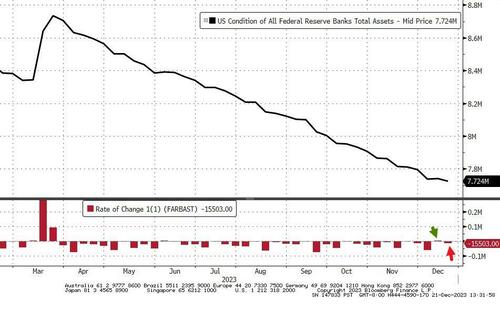

Following the prior week's unexpected $2.2BN rise, The Fed's balance sheet resumed its shrinkage, down $15.5BN last week to a new cycle low...

Source: ZeroHedge

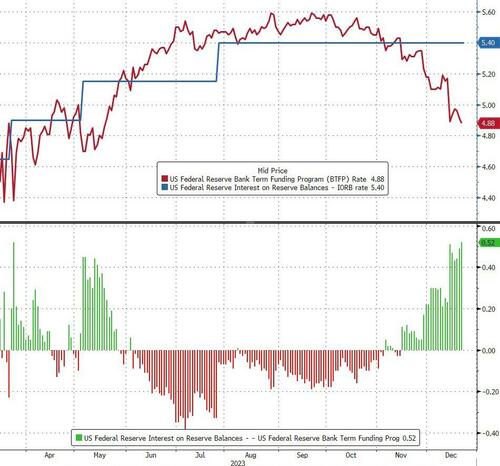

Usage of The Fed's BTFP bank bailout facility soared again last week, jumping $7.5BN to $131BN...

Source: ZeroHedge

But Regional Bank shares still don't care...

Source: ZeroHedge

While this is, at first glance, a worry - bans are borrowing more to fill their balance sheet loss holes - there is another possibility.

An arbitrage for banks is growing more attractive thanks to traders who are betting the Fed will aggressively cut interest rates in 2024.

The rate on the Fed’s Bank Term Funding Program - which allows banks and credit unions to borrow funds for up to one year, pledging US Treasuries and agency debt as collateral valued at par - is the one-year overnight index swap rate plus 10 basis points.

That figure is currently 4.88%, down from 5.17% on Dec. 13.

For institutions that have an account at the Fed, they can borrow from the BTFP at 4.88% and park that at the central bank to earn 5.40% - the interest on reserve balances.

The 52bp spread matches the widest level since the Fed introduced the facility to support a struggling banking system after the collapse of California’s Silicon Valley Bank and Signature Bank in New York.

Source: ZeroHedge

Finally, equity market caps continue to soar after recoupling with bank reserves at The Fed (though the stalling in the drawdown of the RRP has slowed the expansion this week)...

Source: ZeroHedge

Zooming in, it's clear what drove the melt-up, and something just changed...

Source: ZeroHedge

Of course, with The Fed's massive pivot yesterday, sending yields plummeting, regional bank balance sheets may be rescued... for now. Until the next wave of inflation hits...

Originally published by: Tyler Durden on ZeroHedge

The financial market is crumbling and EVERYONE will be affected. Only those who know what's going on and PREPARE will survive... dare we say thrive. Our 7 Simple Action Items to Protect Your Bank Account will give you the tools you need to make informed decisions to protect yourself and the ones you love.