De-Dollarization and Your Bank Account: What You Need to Know

If de-dollarization reaches a point where a critical mass of nations stop using the US dollar as the global reserve currency, your bank deposit could be at risk. Here are a few key possibilities:

1. Currency Devaluation

If the US dollar loses its grip on global trade and as the world’s go-to currency, demand for it will fall—fast. That means a weaker dollar compared to other currencies. And with a weaker dollar, the cost of imports rises. Everyday essentials, from groceries to gas, would cost more. The bottom line? Your savings start to shrink in value. The dollars sitting in your bank account will buy less and less. That’s how inflation creeps in and quietly eats away at your purchasing power.

2. Inflation Will Hit Hard

De-dollarization will invariably lead to high inflation, and when it does, the Fed will scramble to hike interest rates to keep things from spiraling. Sure, higher rates might boost returns on your savings or CDs, but the downside can be even more damaging. If inflation races ahead of those rate hikes, your so-called “increased” savings won’t mean much. Your money will still be worth less. You'll have more dollars, but they’ll buy fewer things. This is the kind of squeeze that hits without mercy. Worst-case scenario: if everyone loses faith in the currency, inflation can easily and quickly transform into hyperinflation.

3. Dollar Liquidity Issues

If the world moves away from using the US dollar in trade, we could face a liquidity crisis. Fewer dollars circulating globally means banks could struggle to maintain their operations smoothly. This could turn into a full-blown crisis, especially for banks that depend on easy access to dollars. In extreme cases, banks’ balance sheets could take a hit, potentially threatening their solvency. And while the Federal Reserve might step in to stop a meltdown, that intervention would come too late for those caught in the middle.

4. Bank Stability and FDIC Insurance

De-dollarization could put real strain on the US economy, and banks—especially smaller, regional ones—could feel the heat. Changes in currency flows, rising inflation, and fluctuating interest rates could make it hard for these banks to stay stable. If there’s an economic downturn, they’ll be the first to buckle. The FDIC insurance may still cover you up to $250,000, but your dollars may not be worth much by the time you’ve recovered your funds. Your money’s value is only as good as its purchasing power—and in this particular scenario, much of that will be gone.

5. Currency Controls or Policy Changes

If the country is facing severe economic instability, don’t be surprised if the government steps in with currency controls such as limits on how much cash you can withdraw from your own bank account. Picture this: you need to access a large sum, and suddenly you're told no. The same could apply to converting dollars for international travel or investments—good luck if you plan to move your money freely. While this might seem extreme, when economies crack, governments tighten their grip. Your financial freedom could be the first casualty.

6. Shift to Digital or Alternative Currencies

There will likely be a push for alternatives—Central Bank Digital Currencies (CBDCs). Banks might start pushing savings accounts in these (or other) forms of money, dangling them as a hedge against dollar instability. But tread carefully. CBDCs bring a whole new set of risks, and if you’re not familiar with how they work, your savings could be in jeopardy. What looks like a smart move could end up being a dangerous gamble, locking you into a system that’s not only full of uncertainty but fully under the government’s surveillance and control.

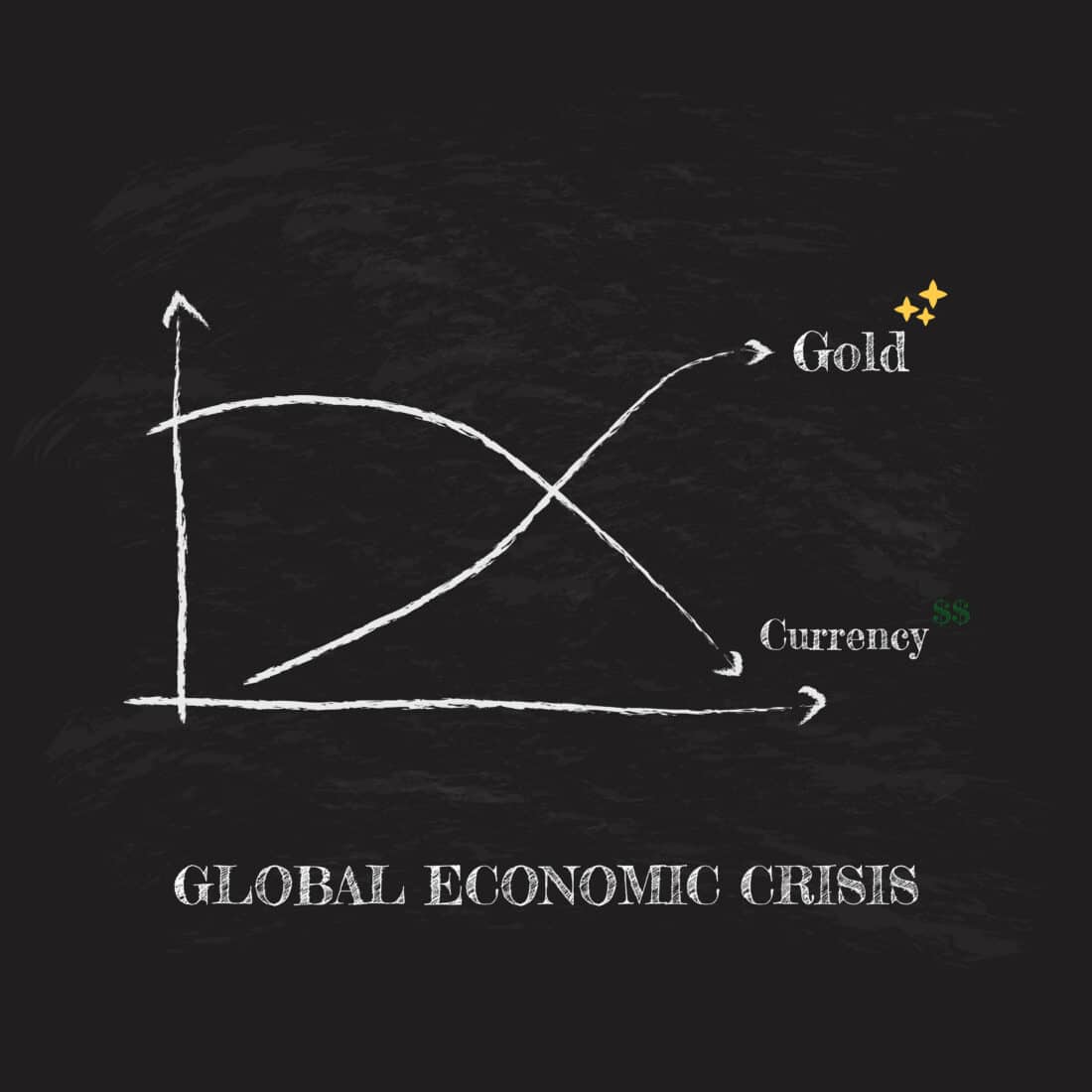

How Physical Gold and Silver Can Help You Navigate This Crisis

Should de-dollarization cause significant dollar devaluation and rising inflation levels, physical gold and silver offer a hedge against currency instability. Unlike fiat currency, gold and silver have intrinsic value that’s recognized across the globe. As the US dollar weakens and prices for goods rise, your gold and silver holdings will likely hold or increase in value, offering you a lifeline when your dollars are worth less.

These precious metals aren’t subject to the same liquidity risks as bank savings. While banks may struggle with access to dollars, gold and silver retain their value independently of any government or central bank intervention. In times of extreme economic instability, when currency controls could lock you out of your own money or push you into uncertain digital alternatives like Central Bank Digital Currencies (CBDCs), having physical gold and silver in your possession means you control your wealth, not the government or a financial institution.