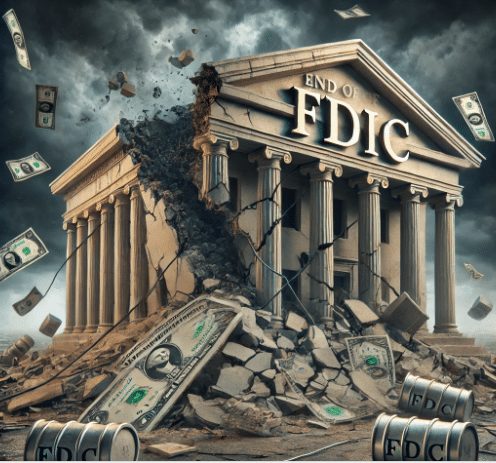

The End of Deposit Insurance? What Trump’s FDIC Overhaul Means for Your Savings

The FDIC in the Crosshairs: What’s Happening?

The Federal Deposit Insurance Corporation (FDIC), a cornerstone of public confidence in the banking system since the Great Depression, may soon be history—or at least fundamentally restructured. Advisors to President-elect Donald Trump are reportedly exploring ways to consolidate or eliminate the FDIC, signaling a bold new era of financial deregulation.

To fully grasp the gravity of this proposal, consider the FDIC’s primary role: insuring deposits up to $250,000 per depositor, per bank. Its very existence has staved off panic and ensured stability, even during the chaos of the 2008 financial crisis. But as deregulation gains traction, what happens when that safety net is removed?

Wall Street’s Celebration vs. Main Street’s Anxiety

The prospect of loosening financial oversight has Wall Street salivating. Deregulation often translates to increased profits and reduced bureaucratic hurdles for the financial elite. But for the average depositor, it raises a troubling question: without federal insurance, what protects your savings in the next banking collapse?

Recent history should give us pause. In the past two years alone, the collapse of Silicon Valley Bank, Signature Bank, and others rattled public confidence. If the FDIC had not stepped in to stabilize these crises, the fallout could have been catastrophic. Now, with the FDIC itself potentially on the chopping block, who bears the risk? You do.

Why Abolish the FDIC?

Critics of the FDIC argue that it distorts the free market by encouraging reckless banking practices, known as moral hazard. If banks know their deposits are insured, they may take excessive risks, confident that taxpayers will foot the bill. This argument, while not entirely unfounded, overlooks the broader societal benefits of deposit insurance.

The Trump transition team, reportedly guided by figures like Tesla CEO Elon Musk and Vivek Ramaswamy, sees an opportunity to streamline—or gut—regulatory agencies. Their vision? Fold deposit insurance into the Treasury Department, or remove it altogether. But the consequences of such a move could be far-reaching and irreversible.

The Real Agenda Behind Deregulation

Let’s ask the uncomfortable question: who benefits from dismantling the FDIC? Certainly not the average American. Deregulation disproportionately favors the financial elite, who thrive in chaos while everyday citizens bear the brunt of market volatility. Could this be another step toward consolidating power among those already at the top?

How to Protect Yourself Now

In an age of regulatory uncertainty, financial sovereignty has never been more critical. Here’s how to safeguard your assets:

- Diversify Beyond Banks: Consider allocating funds to physical gold, Bitcoin, or other decentralized assets immune to traditional banking risks.

- Know Your Bank’s Stability: Research the financial health of your bank and its exposure to high-risk lending.

- Limit Large Deposits: Avoid keeping sums above $250,000 in any one institution—insured or not.

The Final Word: A System at Risk

The abolition of the FDIC would represent more than a regulatory shift; it would signify a fundamental realignment of trust and risk in the financial system. While Wall Street might celebrate, the implications for ordinary Americans could be devastating.

Don’t wait for the system to fail you. Equip yourself with the tools to navigate these uncertain times:

- Claim your free digital book, “Seven Steps to Protect Your Bank Accounts,” here.

- Secure your discounted copy of “The End of Banking as You Know It” here.

Remember, the time to act is before the storm hits. Are you prepared?

The financial market is crumbling and EVERYONE will be affected. Only those who know what's going on and PREPARE will survive... dare we say thrive. Our 7 Simple Action Items to Protect Your Bank Account will give you the tools you need to make informed decisions to protect yourself and the ones you love.