The Job Market is Dead—What Does That Mean for Your Prospects?

The Job Market is Dead—and You're Next

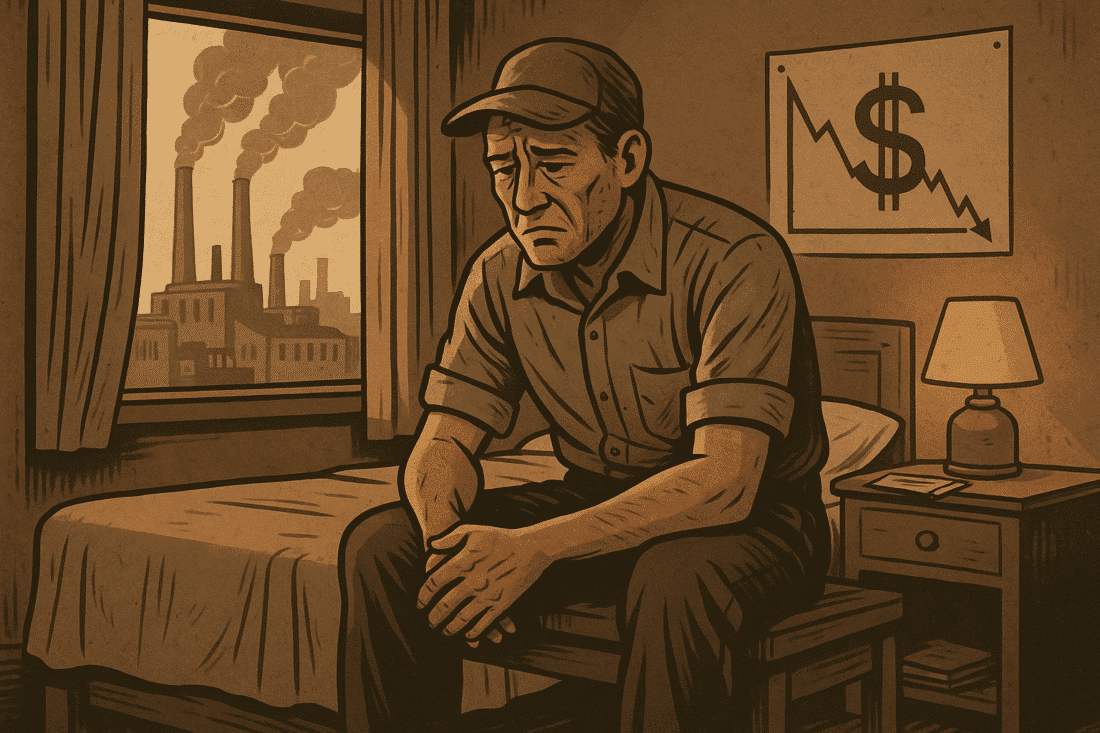

How would you feel if you threw 900 Hail Marys into the void and not one came back? That’s not a rhetorical question—it’s a real-life hell that Jennifer Smith, a 46-year-old mother of three, is living right now in Florida’s economic wasteland. After being laid off from a financial-services gig last September, she’s fired off 900 job applications. One interview. Zero offers. Her severance is circling the drain, and her health insurance premiums are a ticking time bomb.

This isn't bad luck. It's systemic collapse.

Smith isn’t some unqualified slouch. She led a user-experience team. But in 2025’s economic apocalypse, that doesn’t matter. She's now selling her five-bedroom house and downsizing like tens of thousands of others who are realizing that the “American Dream” is just propaganda fed to keep you docile.

Take a deep breath. Because it gets worse.

Highly Skilled and Totally Disposable

Out in Sandpoint, Idaho, 61-year-old software engineer John Comber has applied to 500 jobs since late 2023—same story, no bites. This guy was hoping to ride out one more decade of productive work. Instead, he’s been ghosted by the very industry that once treated him like a rock star. Now, he calls himself “semiretired,” a euphemism for "economically discarded."

And these aren’t isolated cases. They're canaries in the coal mine.

According to the latest data, more than 1.8 million Americans have been unemployed for over 27 weeks—the highest level since 2017 if you ignore the pandemic spike. Median unemployment time has jumped from 9.5 weeks to 10.2. That’s the median, folks. And job cuts? Over 806,000 announced this year alone—a 75% spike compared to the same period in 2024.

We're not sliding into a recession—we're sprinting into it.

Debt: The Silent Killer

And what do most people do when the paychecks stop? They take out loans. Credit cards, payday advances, personal lines of credit. We're now sitting on over $18 trillion in household debt—about $53,000 for every man, woman, and child. Most folks don’t even admit they’re drowning. Two-thirds of debtors lie or hide their financial situation from family and friends. Why? Shame. Embarrassment. The illusion that financial struggle is a personal failure instead of the result of a rigged economic game.

This financial deception doesn’t just damage bank accounts—it destroys relationships, mental health, and any chance of meaningful solidarity. That’s by design. Divide and conquer.

The Housing Market’s Collapse Signals What’s Next

Now, zoom out.

Residential investment dropped 1.3% in Q1, then cratered another 4.6% in Q2. Ed Leamer warned us years ago—residential investment is the canary. And it’s dead. Home sales? The lowest since 2012. Spring—once the goldmine for real estate—is now a ghost town. And if the housing market is toast, the rest of the economy isn't far behind.

This is what economic erosion looks like. It’s not sudden. It’s engineered over decades. Inflation, currency devaluation, regulatory capture, and digital dependency—all designed to squeeze the middle class until it evaporates.

You're Running Out of Time

So if you’re still employed, don't get too comfortable. The walls are closing in, and next time, it could be you applying for hundreds of jobs in a system that’s designed to ignore you.

Wake up. Unplug. Prepare.

Download Seven Steps to Protect Yourself from Bank Failure by Bill Brocius before it’s your name on the list.