Digital Dollar EXPOSED: FedNow, Stablecoins, and the Quiet Rise of Programmable Money Control

The Distraction: “CBDCs Are Banned—You’re Safe”… Right?

You’ve probably seen the headlines—politicians signaling opposition to central bank digital currencies (CBDCs), positioning themselves as defenders of financial freedom.

But here’s the uncomfortable reality: you don’t need an official CBDC rollout to build a CBDC-style control system.

While some policymakers have voiced resistance to a formal digital dollar, the infrastructure that makes it possible—real-time settlement systems like FedNow, expanded financial surveillance, and programmable payment layers—is already being deployed.

The game isn’t about labels. It’s about capabilities.

And those capabilities are coming online fast.

The Financial API State: When Money Becomes a Controlled Interface

What you’re watching emerge is what I call the Financial API State—a system where money isn’t just stored or transferred, it’s managed through programmable interfaces controlled by institutions.

Think about how platforms like Apple or Google control apps:

- They set the rules

- They approve or deny access

- They monitor behavior

- They can revoke privileges instantly

Now apply that model to your money.

With systems like the FedNow payment system, transactions move instantly—but they also become traceable, interceptable, and conditionally allowed.

This isn’t theoretical. It’s infrastructure.

And once money runs through APIs, it can be:

- Filtered

- Flagged

- Delayed

- Denied

Not by a human. By a rule set.

Transaction-Level Governance: Control at the Point of Purchase

Here’s where it gets personal.

The old system controlled accounts. The new system controls transactions.

That means:

- Not “you’re banned from banking”

- But “this specific payment isn’t allowed”

Welcome to transaction-level governance.

Every payment becomes a decision point:

- Is this vendor approved?

- Does this purchase align with policy?

- Has this user triggered any flags?

No need to freeze your account when they can just quietly say:

“Transaction declined.”

No explanation. No appeal. Just friction.

Soft Financial Lockdowns: Control Without Headlines

This is the part most people miss.

Control won’t come with dramatic announcements. It will come through soft financial lockdowns.

No official bans. Just:

- “Temporary restrictions”

- “Compliance checks”

- “Security reviews”

- “Processing delays”

You’ll still have access to your money.

You just won’t be able to use it freely.

That’s the genius of it—it avoids panic while achieving the same end result.

A cashless society doesn’t need force if it can rely on invisible constraints.

Behavior-Linked Currency: When Money Watches You Back

Now we get to the endgame: behavior-linked currency.

This is where spending power becomes tied to:

- Identity

- Reputation

- Activity

- Compliance

It doesn’t have to be called a “social credit system” to function like one.

Imagine:

- Higher scrutiny based on your transaction history

- Spending limits based on “risk profiles”

- Access shaped by your digital identity footprint

This is where programmable money stops being a convenience and starts becoming a lever of control.

Stablecoins: The Shadow CBDC Nobody’s Questioning

Here’s the twist most people aren’t ready for:

Even if a formal CBDC rollout stalls or gets blocked politically, stablecoins can serve as a parallel path.

They’re marketed as:

- Private

- Decentralized-adjacent

- Dollar-backed alternatives

But in reality, many stablecoins:

- Depend on centralized issuers

- Require regulatory compliance layers

- Operate within the same financial rails

That makes them the perfect “shadow CBDC”—familiarizing users with:

- Digital wallets

- Tokenized dollars

- Programmable transfers

All without triggering the same resistance as a government-branded CBDC.

It’s not about replacing the system overnight.

It’s about training people to accept it incrementally.

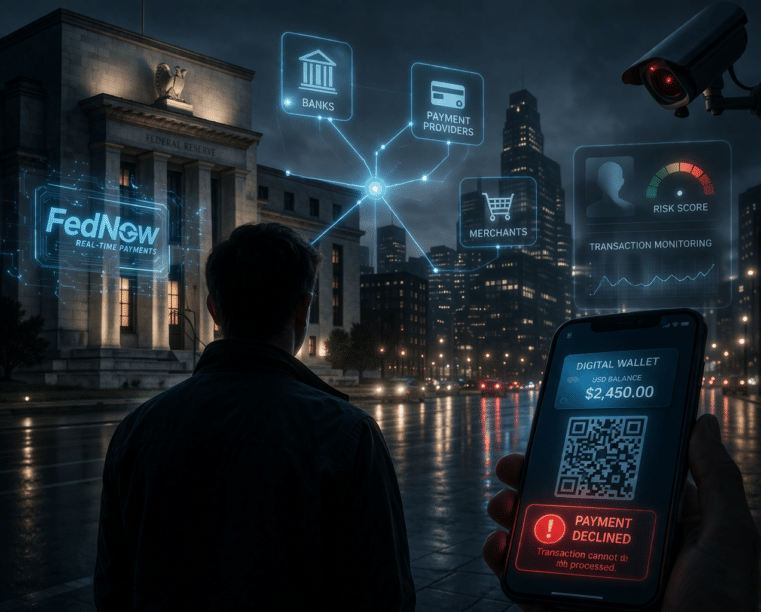

FedNow: The Backbone of Real-Time Financial Control

Let’s talk about FedNow.

On paper, it’s just a faster payment system—instant transfers, 24/7 availability.

But speed isn’t the real story.

Control is.

Because real-time systems enable:

- Immediate enforcement of rules

- Instant visibility into transactions

- Continuous monitoring of financial activity

When combined with API-driven controls, FedNow becomes more than infrastructure—it becomes a control layer.

And once that layer is normalized, adding programmability is just a software update away.

The Bigger Picture: This Isn’t About Technology—It’s About Power

None of this is inherently evil in isolation.

Faster payments? Useful.

Digital currency? Efficient.

Fraud prevention? Necessary.

But when you connect the dots:

- Financial API State

- Transaction-level governance

- Soft financial lockdowns

- Behavior-linked currency

You don’t get innovation.

You get a system capable of total financial oversight and selective restriction.

And once that system is fully operational, reversing it won’t be simple.

Because by then, it won’t feel like control.

It will feel like normal.

My Take: This Is the Transition Phase—And Most People Don’t See It

What concerns me isn’t a sudden rollout.

It’s the gradual normalization.

People are being walked into:

- Cashless habits

- Digital wallets

- Platform-mediated money

By the time the rules tighten, the infrastructure will already be in place—and widely accepted.

That’s how systems like this succeed.

Not through force.

Through familiarity.

The Bottom Line: Prepare Now or Adapt Later—On Their Terms

You don’t have to agree with every angle here.

But ignoring the trajectory? That’s a mistake.

Because whether it’s called:

- FedNow

- Stablecoins

- Digital dollar

- Or something else entirely

The direction is clear: more visibility, more control, more programmability.

And less financial autonomy.

Your Next Move (This Isn’t Optional)

If you’re starting to see where this is heading, then you need to act accordingly.

That means understanding:

- How programmable money actually works

- Where the control points are

- And what you can do—right now—to protect your financial independence

Download the Digital Dollar Reset Guide by Bill Brocius. This isn’t theory—it’s practical intelligence for navigating what’s coming.

Because once this system is fully locked in, options won’t expand.

They’ll shrink.