The U.S. Treasury’s Hidden Insolvency Signals the Coming Loss of Financial Freedom

The Numbers Aren’t Just Bad—They’re Systemic

Let’s strip this down to brass tacks.

The Treasury’s own books show:

- $6.06 trillion in assets

- $47.78 trillion in liabilities

That’s not “concerning.” That’s a structural fracture.

In the real world—outside the protected bubble of government—those numbers signal collapse. No bank survives it. No corporation escapes it. But governments don’t play by those rules.

They rewrite them.

And that’s where this gets dangerous for you.

Governments Don’t Go Bankrupt—They Restructure Reality

You’ll hear the usual defense: “The U.S. can’t go bankrupt—it prints its own currency.”

Technically accurate. Practically deceptive.

What actually happens is more subtle—and far more dangerous:

- Currency debasement (your dollar buys less every year)

- Persistent inflation (not a spike—an engineered baseline)

- Tax expansion (visible and hidden)

- Financial repression (your savings quietly trapped and diluted)

This isn’t collapse. It’s controlled demolition.

And the cost doesn’t hit the system.

It hits you.

The Real Liability Bomb: Unfunded Promises

The headline debt is just the surface.

Buried underneath are obligations that make the official numbers look tame:

- Social Security

- Medicare

- Federal pensions

These aren’t funded. They’re projected. Assumed. Kicked down the road.

And here’s the problem: the math only works under perfect conditions—strong growth, stable demographics, low interest rates.

We don’t have any of those.

Instead, we have:

- An aging population

- Rising interest costs

- Slowing economic momentum

That’s not a stable system. That’s a pressure cooker.

The Audit Failure No One Wants to Talk About

Here’s where it crosses from reckless to absurd:

The U.S. government cannot pass a clean audit.

Let that land.

The largest financial entity on Earth:

- Cannot fully verify its books

- Cannot guarantee internal controls

- Repeatedly fails audit standards

If this were a private institution, regulators would shut it down overnight.

In Washington? It’s filed away and ignored.

Why This Was Buried

This story didn’t disappear by accident.

It disappeared because it breaks the narrative.

You can’t:

- Sell economic stability

- Justify endless spending

- Maintain consumer confidence

…while admitting the system is mathematically unstable.

So the report gets released quietly.

No headlines. No deep dives. No accountability.

Meanwhile, the underlying problem keeps expanding.

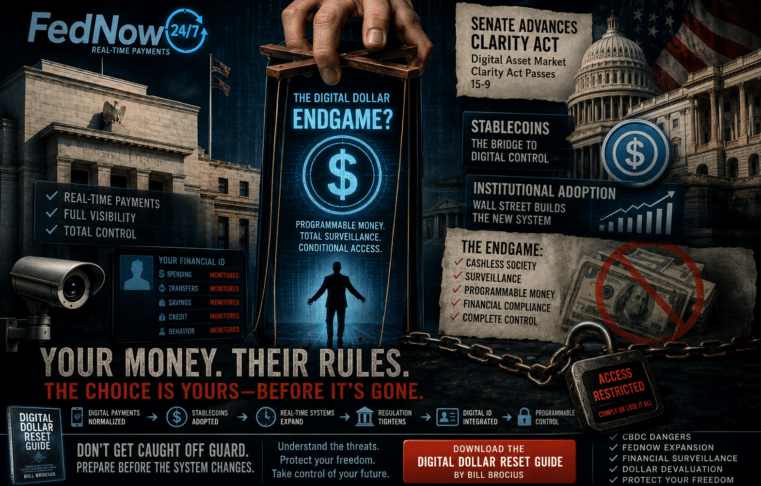

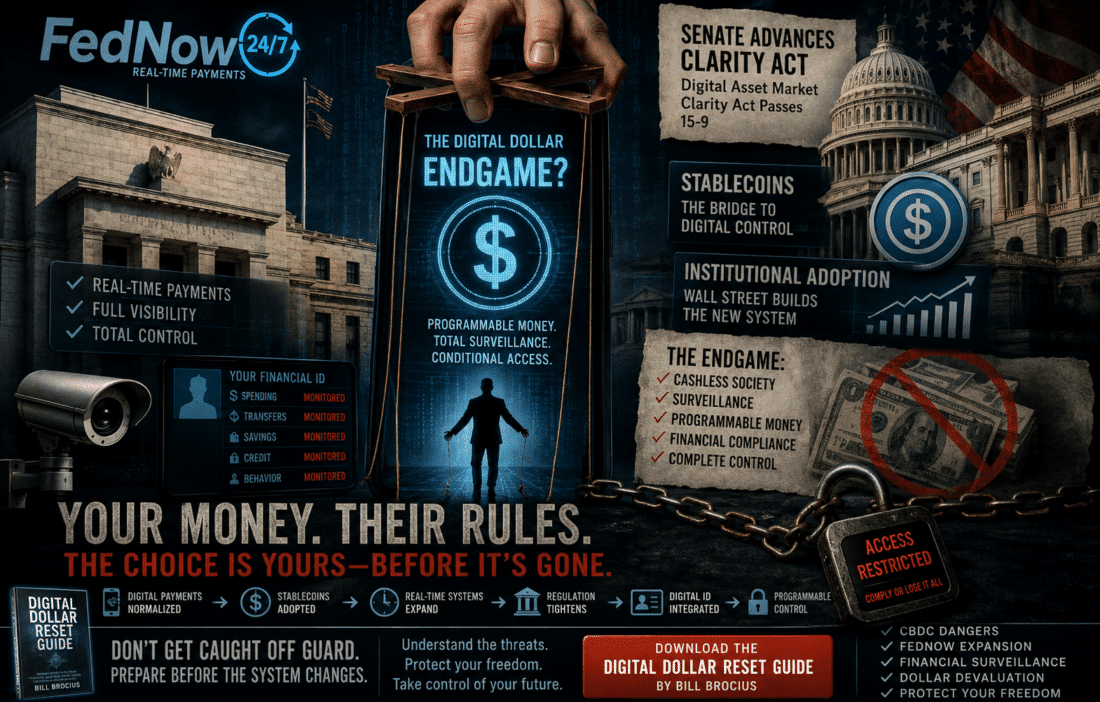

Enter FedNow: The Infrastructure for Control

Now we connect the dots.

When a system becomes financially strained, it doesn’t just adjust policy—it builds control mechanisms.

That’s where FedNow enters the picture.

Marketed as a faster payment system, FedNow is something else entirely:

- Real-time transaction capability

- Centralized oversight potential

- Foundation for programmable money

This isn’t speculation. It’s architecture.

And it aligns perfectly with what comes next.

CBDCs and Programmable Money: The Endgame

Central Bank Digital Currencies (CBDCs) are already being tested globally.

What makes them different?

Control.

With programmable money, authorities can:

- Track every transaction

- Limit how money is spent

- Expire funds to force consumption

- Enforce compliance through financial access

Pair that with a financially strained system, and the incentive becomes obvious:

Control replaces stability.

Instead of fixing the imbalance, the system manages behavior.

Financial Surveillance Becomes the Default

This is where “convenience” turns into constraint.

A fully digital monetary system enables:

- Continuous transaction monitoring

- Automated enforcement of financial rules

- Integration with policy decisions in real time

No warrants. No friction. No delay.

Just silent oversight embedded into the system itself.

The Quiet Shift to a Cashless Society

Cash is the one thing that still operates outside centralized control.

That’s why it’s being phased out—slowly, quietly, deliberately.

We’re already seeing:

- Reduced cash usage

- Digital-only incentives

- Payment ecosystem consolidation

A cashless society isn’t about innovation.

It’s about visibility.

What This Means for You

This isn’t theoretical. It’s already unfolding.

You’re feeling it through:

- Rising costs that never fully retreat

- Savings that don’t keep up

- Financial systems that feel increasingly restrictive

And what’s coming next amplifies all of it:

- Less privacy

- Less control

- Less flexibility

More structure. More oversight. More dependency.

My Take: This Isn’t Collapse—It’s Conversion

Let’s be clear.

This system isn’t falling apart overnight.

It’s being transitioned.

From:

- Open financial movement

- Decentralized cash usage

- Limited oversight

To:

- Controlled digital systems

- Programmable currency

- Embedded financial surveillance

The Treasury numbers aren’t just a warning.

They’re the justification.

Final Word: Don’t Wait for the Announcement

You won’t get a press conference saying:

“Financial freedom is being restructured.”

You’ll get:

- New systems (like FedNow)

- New policies

- New limitations framed as improvements

By the time it’s obvious, it’s already locked in.

The Only Rational Move Now

If you see what’s happening, you don’t ignore it.

You prepare.

That means understanding:

- How digital currencies like CBDCs actually work

- What FedNow enables long term

- How financial surveillance expands from here

- And most importantly—how to position yourself before the system tightens

This isn’t optional anymore.

It’s required intelligence.

Download the Digital Dollar Reset Guide Here

Because once programmable money becomes the standard, adapting late won’t be an inconvenience—it’ll be a liability.