FedNow, CBDCs, and the Quiet Balance Sheet Reset: How the Fed Is Rewiring Financial Control Behind the Scenes

The Fed’s Balance Sheet Isn’t Just Big—It’s a Control Mechanism

Let’s cut through the polite language.

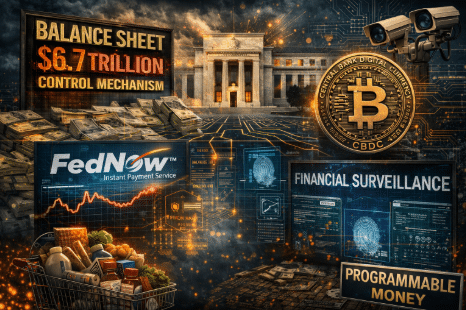

When economists talk about the Fed’s $6.7 trillion balance sheet, they frame it like a technical problem—too many assets, too many reserves, time to “normalize.”

But here’s the reality:

That balance sheet is a direct lever of control over the financial system.

Before 2008, the Fed was a background player—about $900 billion in assets, barely 6% of GDP. Today? It’s north of 20% of GDP, embedded in everything from mortgage-backed securities to emergency lending facilities.

That’s not just growth. That’s dependency.

Markets don’t just react to the Fed anymore—they rely on it.

Kevin Warsh’s Plan: Shrink the System Without Breaking It

Kevin Warsh wants to reduce the Fed’s footprint. On paper, that sounds like a return to sanity.

But the article makes one thing crystal clear:

You can’t just shrink the balance sheet without consequences.

Why?

Because those assets are tied directly to bank reserves—the digital dollars banks park at the Fed. Pull assets out too fast, and you drain reserves from the system.

That’s where things get dangerous.

We’ve seen this before. In 2019, the Fed tried tightening. Money markets seized up. Liquidity vanished overnight. The system buckled—and the Fed had to step back in.

Translation:

The system is addicted.

The Real Problem: Banks Are Hooked on Fed Reserves

Stanford economist Darrell Duffie lays it out plainly:

Shrinking the balance sheet only works if you reduce demand for reserves.

That’s the key insight most people will miss.

Banks don’t just hold reserves—they depend on them for:

- Liquidity requirements

- Payment settlement

- Risk management

- Regulatory compliance

So if the Fed wants to shrink its balance sheet, it has to retrain the entire banking system to operate with less reliance on central bank money.

That’s not a tweak. That’s a transformation.

The Quiet Shift Toward a New Financial Architecture

Look at the proposed solutions:

- Adjust regulations so banks don’t need as many reserves

- Redesign payment systems

- Penalize excess reserves with tiered interest

- Actively manage liquidity shocks

On the surface, that’s policy fine-tuning.

Underneath?

That’s the blueprint for a fully engineered financial system—one where:

- Liquidity is centrally managed

- Incentives are algorithmically controlled

- Money flows are monitored and adjusted in real time

Sound familiar?

It should.

This is the same infrastructure required for central bank digital currencies (CBDCs) and systems like FedNow.

FedNow and the Rise of Programmable Money

The FedNow payment system is already live. It enables instant, 24/7 settlement between banks.

That might sound convenient. But here’s what it really does:

- Eliminates friction in money movement

- Reduces the need for traditional reserve buffers

- Centralizes transaction visibility

Now connect the dots.

If banks need fewer reserves because transactions settle instantly…

And the Fed controls the infrastructure…

And digital currency layers get added on top…

You don’t just get efficiency.

You get programmable money.

Money that can be:

- Tracked

- Restricted

- Timed

- Conditional

That’s not theory. That’s where this is heading.

Financial Surveillance Is the Missing Piece They Don’t Talk About

Here’s what’s conveniently absent from the mainstream discussion:

When you centralize reserves, payments, and liquidity management, you create a system where every transaction becomes data.

And data becomes control.

A smaller balance sheet doesn’t mean less power.

It can mean more precise power.

Instead of flooding the system with money, the Fed can:

- Target specific sectors

- Influence behavior through incentives

- Adjust liquidity in real time

That’s a shift from blunt force to surgical control.

The Cashless Endgame: Less Cushion, More Control

Reducing reserves might sound like decentralization.

It’s not.

It’s about removing excess buffers in the system—so everything runs tighter, faster, and more dependent on centralized infrastructure.

That’s exactly what a cashless society requires.

No slack. No anonymity. No escape valves.

Just a streamlined system where:

- Every dollar is digital

- Every transaction is visible

- Every participant is accountable to the network

And who runs that network?

You already know the answer.

My Take: This Isn’t Shrinkage—It’s a Reset

Don’t be fooled by the language.

This isn’t the Fed stepping back.

It’s the Fed evolving its control strategy.

From:

- Large, visible interventions

To:

- Subtle, systemic influence

From:

- Expanding the balance sheet

To:

- Rewiring how money itself functions

The danger isn’t that they’re doing too much.

It’s that they’re getting better at doing it quietly.

What This Means for You

If this transition continues, here’s what you’re looking at:

- Reduced financial privacy

- Increased transaction monitoring

- Greater dependence on centralized systems like FedNow

- The eventual rollout of a full-scale digital dollar (CBDC)

And once that system is fully in place?

Opting out won’t be easy.

Final Warning: Prepare Before the System Locks In

You don’t need to panic—but you do need to pay attention.

Because what’s being built right now isn’t just a new monetary policy framework.

It’s a new financial reality.

One where control is embedded into the system itself.

If you’re seeing the warning signs—FedNow expansion, CBDC pilots, balance sheet restructuring—then you already know this isn’t business as usual.

The next step is preparation.

Download the Digital Dollar Reset Guide by Bill Brocius Here

This isn’t optional reading. It’s critical intelligence for anyone serious about protecting their financial autonomy in a world of programmable money and expanding financial surveillance.

The system is changing.

The only question is whether you’re ready for it.