FOMC Minutes Show Just How Worried the Fed is About Inflation

Nearly all members of the Federal Open Market Committee (FOMC) still believed it would be appropriate to cut rates this year, and they also favored cutting the pace of monthly asset runoff by 50%, but some cautioned that recent rises in inflation were broad-based and not ‘noise’, according to the minutes from the March 19 - 20 meeting released Wednesday afternoon.

In their discussion on the policy outlook, “participants judged that the policy rate was likely at its peak for this tightening cycle, and almost all participants judged that it would be appropriate to move policy to a less restrictive stance at some point this year if the economy evolved broadly as they expected,” the minutes read. “In support of this view, they noted that the disinflation process was continuing along a path that was generally expected to be somewhat uneven. They also pointed to the Committee's policy actions together with the ongoing improvements in supply conditions as factors working to move supply and demand into better balance.”

Participants also noted data pointing to “strong economic momentum and disappointing readings on inflation in recent months” and said it would not be appropriate to reduce rates “until they had gained greater confidence that inflation was moving sustainably toward 2 percent.”

The minutes said that members did agree that monetary policy “remained well positioned to respond to evolving economic conditions and risks to the outlook, including the possibility of maintaining the current restrictive policy stance for longer should the disinflation process slow, or reducing policy restraint in the event of an unexpected weakening in labor market conditions.”

Regarding the evolving inflation picture in the United States, The FOMC said significant progress had been made toward the two percent inflation target “even though the two most recent monthly readings on core and headline inflation had been firmer than expected.”

Wednesday morning’s CPI report was the third consecutive firmer-than-expected reading, which has caused many market participants to reassess the timing and the degree of potential rate cuts.

“Some participants noted that the recent increases in inflation had been relatively broad based and therefore should not be discounted as merely statistical aberrations,” the minutes read. “However, a few participants noted that residual seasonality could have affected the inflation readings at the start of the year. Participants generally commented that they remained highly attentive to inflation risks but that they had also anticipated that there would be some unevenness in monthly inflation readings as inflation returned to target.”

In their discussions of the uncertainties around the economic outlook, FOMC members “generally noted their uncertainty about the persistence of high inflation and expressed the view that recent data had not increased their confidence that inflation was moving sustainably down to 2 percent.” The minutes also showed some participants concerned about “geopolitical risks that might result in more severe supply bottlenecks or higher shipping costs that could put upward pressure on prices,” and said this could also impact economic growth.

“The possibility that geopolitical events or surges in domestic demand could generate increased energy prices was also seen as an upside risk to inflation,” they wrote. “Some participants noted the uncertainties regarding the restrictiveness of financial conditions and the associated risk that conditions were or could become less restrictive than desired, which could add momentum to aggregate demand and put upward pressure on inflation.”

During discussions of the Fed’s balance sheet, members “observed that balance sheet runoff was proceeding smoothly,” but “the vast majority of participants thus judged it would be prudent to begin slowing the pace of runoff fairly soon,” with most favoring “reducing the monthly pace of runoff by roughly half from the recent overall pace.”

“[P]articipants generally preferred to maintain the existing cap on agency MBS [mortgage-backed securities] and adjust the redemption cap on U.S. Treasury securities to slow the pace of balance sheet runoff,” the minutes noted.

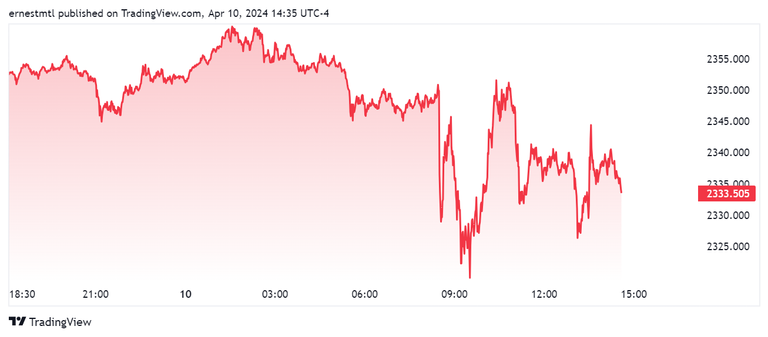

Gold prices appear to have taken the minutes in stride, with only some sideways price action, as markets already adjusted their rate expectations following this morning’s firmer-than-expected CPI readings. Spot gold last traded at $2,333.50 per ounce, down 0.77% on the session at the time of writing.