The Illusion of Progress: Why Median Income Gains Are a Mirage”

💣 The Real Story Behind “Record High” Median Income

The story starts with a shiny headline: “Middle-income households are making more than ever.” That’s technically true — the 2024 real median household income clocked in at $83,730. It’s the highest on record.

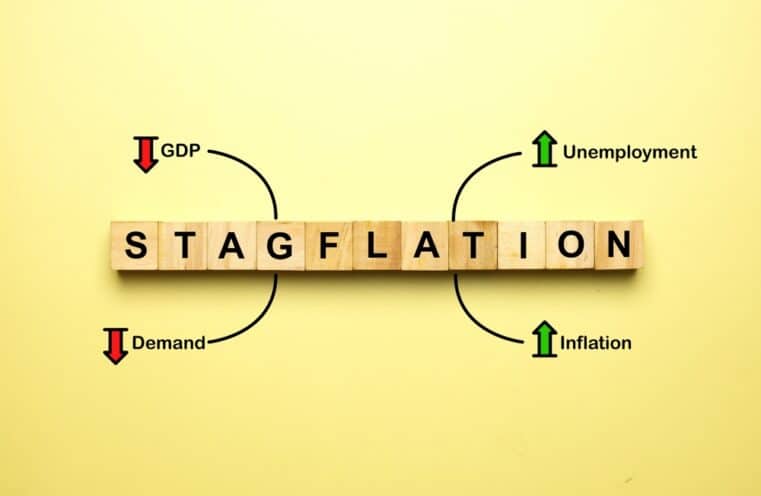

But here’s the kicker: that “record” is mostly meaningless without context. The Census Bureau itself admits the 2024 figure is not statistically different from 2023 or even 2019. Translation? Household income isn’t meaningfully growing — it’s barely surviving inflation. Meanwhile, costs for essentials — housing, food, insurance, education — continue climbing like a slow-motion financial death march.

Even worse, these averages hide deep inequalities. Income rose for Asian and Hispanic households, fell for Black households, and stagnated for White households. Women working full-time earned less than in previous years. So whose median is this, exactly? Averages are for economists. Real people live on margins.

🧨 Mortgage Rates and the Debt Time Bomb

We’re also being told to cheer because 30-year mortgage rates dropped from 8% to about 6.2%. That’s supposed to be “good news.” But compared to what? In the cheap-money era of 2010–2020, Americans refinanced homes at 2–3%. Today’s rates are still double that. And let’s not forget: home prices didn’t fall. They rose.

So while rates moderated, the total cost of borrowing — especially for first-time buyers — is brutal. This is how the Fed tightens the screws. Interest rate “normalization” sounds neutral — but in practice, it means the average family pays hundreds more a month just to keep a roof over their heads.

🧠 Why This “Growth” is Financial Theater

This isn’t economic health — it’s performance art. The Treasury issues debt like confetti while pretending deficits don’t matter. The Fed talks about inflation like it’s under control, even as grocery bills and insurance premiums devour paychecks. Meanwhile, the financial class — flush with cash and central bank backstops — just keeps flipping assets, extracting rent, and raking in profits from your labor and loans.

And yet the official line is always the same: “The overall trajectory is pretty darn solid.”

Solid for who?

It’s not solid for the family in Phoenix scraping together a $2,400 mortgage on a starter home. It’s not solid for the nurse in Atlanta buried under student loans and inflation. And it sure as hell isn’t solid for the millions of Americans whose “middle class” dream is now just one medical bill, layoff, or car repair away from collapse.

🔍 Connect the Dots: FedNow, CBDCs, and the Centralized Trap

Let’s not forget the broader machinery at play. These income numbers — even if they were impressive — won’t protect you from what’s coming: programmable digital currencies (hello, FedNow), centralized economic surveillance, and the erosion of cash-based autonomy. This whole system is moving toward total financial control — and the median income stat is just the cheese in the trap.

When the next “crisis” hits, they’ll sell you safety in the form of digital wallets, UBI with strings, and biometric access to your own savings. All built on the back of control and compliance.

You want freedom? It doesn’t come from higher income on a government spreadsheet. It comes from self-reliance, decentralization, and opting out of their game.

⚠️ Call to Action: Don’t Be Fooled — Be Ready

Want to see through the fog and protect what’s yours before the next wave hits? Download “Seven Steps to Protect Yourself from Bank Failure” by Bill Brocius. This guide will give you the knowledge and tools you need to stay solvent, stay secure, and stay free — no matter how rosy the headlines look.

—

This isn’t just an economic story. It’s a warning shot. They want you complacent. Don’t give them the satisfaction.