PRIVATE CREDIT PANIC: The Quiet Bank Run They Don’t Want You to See Before It Spreads

The “Bank Run” Nobody Wants to Call a Bank Run

Let’s drop the polite language.

When nearly 41% of investors in a fund demand their money back at once, that’s not “elevated redemptions.” That’s a run.

Blue Owl—one of the biggest players in private credit—just hit that wall. Hard.

Their Technology Income Corp fund saw 40.7% of investors head for the exit. Another flagship fund saw requests jump to 21.9%. Those are not normal numbers. Those are panic numbers.

And what did Blue Owl do?

They slammed the brakes.

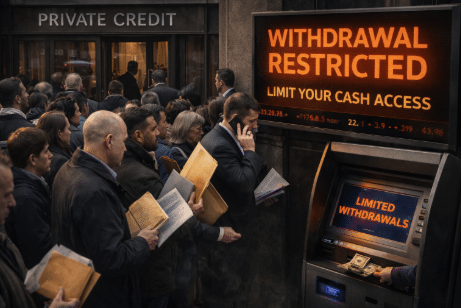

Redemptions capped. Withdrawals limited. Access restricted.

If this were your local bank, people would be lined up around the block.

The Illusion of Liquidity Just Got Exposed

Private credit has always sold a carefully crafted story:

- Higher yields

- Stable returns

- Less volatility than public markets

What they didn’t emphasize?

You don’t get your money back when you want it. You get it when they let you.

That’s not a bug. That’s the design.

These funds operate in a world where assets aren’t easily sold. Loans to mid-sized companies. Illiquid deals. Complex structures. When everyone wants out at once, there’s no natural buyer waiting on the other side.

So what happens?

They gate withdrawals.

Exactly like we just saw.

The “Sell the Good Stuff First” Problem

Back in February, Blue Owl tried to stay ahead of the storm.

They sold off $1.4 billion in loans to meet redemption demand. Sounds responsible—until you look closer.

Those weren’t random assets.

They were likely the best assets—the ones buyers would actually take.

Which leaves behind what?

The leftovers. The riskier loans. The stuff nobody wants.

That’s the dirty secret of forced selling:

The stronger your portfolio looks on paper, the weaker it may actually be underneath.

And investors aren’t stupid. They saw the move. They connected the dots. And then they ran.

Financial Engineering Meets Reality

Here’s where things get even more uncomfortable.

Some of those loan sales? Done at near face value—99.7 cents on the dollar—and allegedly involving related parties.

Translation:

They may have been propping up valuations just long enough to avoid panic.

But markets have a way of sniffing that out.

Once confidence cracks, it spreads fast.

And now we’re watching that play out in real time.

This Isn’t Just One Firm—It’s an Entire Industry

Private credit isn’t small anymore.

We’re talking about a $1.8 trillion market.

And Blue Owl isn’t alone. Other giants—Apollo, BlackRock, Ares—are all operating under similar structures:

- Limited liquidity

- Redemption caps

- Illiquid underlying assets

So when one major player starts gating withdrawals, it raises a dangerous question:

Who’s next?

Because if this becomes a pattern, we’re not looking at isolated stress.

We’re looking at systemic pressure.

The Bigger Risk Nobody’s Talking About

Here’s what should actually concern you.

Private credit has quietly become the lifeline for thousands of companies—especially smaller tech firms and mid-sized businesses that can’t access traditional bank loans.

If that funding dries up?

- Companies can’t refinance debt

- Payrolls get squeezed

- Expansion plans collapse

- Layoffs follow

This doesn’t stay in some niche corner of finance.

It leaks out.

Into jobs. Into markets. Into the broader economy.

Institutional Investors Are Already Moving

One detail most people missed:

This wasn’t retail panic.

This was driven by large, concentrated investors—the kind with teams of analysts and early access to information.

When they move first, it’s rarely random.

It’s calculated.

And historically, when institutions head for the exits before everyone else notices… they’re usually early, not wrong.

The Narrative vs. Reality Gap

Executives are still saying everything is “resilient.”

They always do.

But here’s the disconnect:

- If fundamentals are strong, why the rush to withdraw?

- If liquidity is stable, why gate redemptions?

- If confidence is intact, why are institutions pulling billions?

You don’t get numbers like this from “negative sentiment.”

You get them when people stop believing the story.

This Is What a Slow-Motion Unwind Looks Like

Crises don’t always explode overnight.

Sometimes they unfold like this:

- Early warnings dismissed

- Liquidity tested

- Redemptions spike

- Withdrawals restricted

- Confidence erodes

- Contagion spreads

We’re somewhere between steps 3 and 4 right now.

And once gating becomes normalized, the psychology shifts.

People stop asking if they can get their money out.

They start wondering when they won’t be able to anymore.

My Take: This Was Always the Weak Link

I’ve been around long enough to recognize the pattern.

Whenever you see:

- Complex structures

- Smoothed returns

- Limited transparency

- Restricted access to your own capital

You’re not looking at stability.

You’re looking at controlled perception.

Private credit worked as long as:

- Money kept flowing in

- Redemptions stayed low

- Nobody tested the system at scale

Now that test is happening.

And the results aren’t encouraging.

Final Thought: Pay Attention to the Doors, Not the Decor

Everyone loves to focus on returns.

Few people ask the only question that matters:

Can I get my money out when I need it?

Right now, in one of the fastest-growing corners of finance, the answer is becoming:

“Not exactly.”

And once that realization spreads, things can move very quickly.

Critical Next Step: Don’t Ignore What This Signals

What’s happening here isn’t just about one firm or one sector—it’s part of a much bigger shift in how money, access, and control are being redefined.

As systems tighten and liquidity becomes conditional, the same mechanisms showing up in private markets are beginning to appear in broader financial infrastructure—especially with the rollout of tools like FedNow and the accelerating push toward central bank digital currencies (CBDCs).

These systems introduce something far more concerning:

- Programmable money

- Transaction-level surveillance

- Centralized control over when and how you can access your funds

If gated funds are the warning shot, what comes next could make those restrictions look minor.

That’s why understanding what’s coming isn’t optional anymore.

It’s critical.

Download the Digital Dollar Reset Guide by Bill Brocius

This isn’t theory—it’s a breakdown of the exact mechanisms being built right now, and what you can do to protect your financial autonomy before the window to act starts closing.