Programmable Money vs Sound Money: The FedNow Digital Dollar Shift They Didn’t Fully Explain

Two Competing Visions of Money

Strip away the noise, and this comes down to a fundamental clash:

- Programmable money — digital, trackable, adaptable by design

- Sound money — physical, finite, independent of centralized control

FedNow didn’t invent this divide—but it accelerates it.

The system represents a leap forward in how quickly money moves. But speed isn’t the only variable that matters. Control, transparency, and ownership are just as critical—and they’re where these two forms of money diverge sharply.

Where FedNow Fits Into the Digital Dollar Equation

FedNow is a real-time payment system. That’s the official line, and it’s accurate as far as it goes.

But systems like this don’t exist in isolation. They’re part of a broader financial architecture that’s evolving toward fully digital rails.

FedNow enables:

- Instant settlement between financial institutions

- Continuous, always-on transaction processing

- Standardized infrastructure connecting banks directly to central systems

On its own, that’s not a central bank digital currency (CBDC). But it does create an environment where a digital dollar could be deployed more easily and efficiently.

In other words, FedNow isn’t necessarily the endpoint—it’s a foundation.

The Defining Feature: Programmability

Here’s where the conversation shifts from convenience to capability.

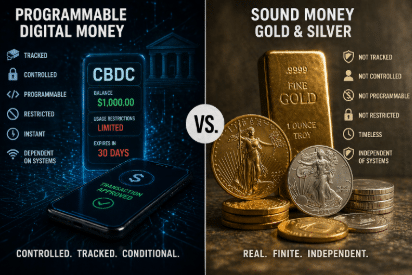

Programmable money isn’t just digital—it’s conditional.

In theory, it can:

- Automate compliance rules

- Restrict how funds are used

- Trigger actions based on predefined conditions

Supporters frame this as innovation—reducing fraud, increasing efficiency, improving policy implementation.

Critics see a different angle: a system where money is no longer neutral, but responsive to external inputs.

That distinction matters.

Traditional currency doesn’t change based on behavior. Programmable systems can.

Sound Money: Why Gold and Silver Still Matter

Gold and silver don’t compete on speed. They compete on independence.

They aren’t:

- Digitally tracked

- Instantly transferable across networks

- Dependent on centralized infrastructure

And that’s precisely the point.

For centuries, these metals have been used as stores of value because they exist outside the control of any single authority. They don’t require permission to hold. They don’t rely on uptime, connectivity, or institutional access.

In a world moving toward increasingly digital financial systems, that difference stands out more—not less.

Financial Surveillance: Capability vs. Intention

Modern banking already involves oversight. That’s not controversial.

What’s changing is the degree and speed of visibility.

With real-time systems:

- Transactions can be processed and analyzed instantly

- Patterns can be identified as they emerge

- Responses can be automated

This doesn’t automatically imply misuse. But it does expand what’s technically possible.

And historically, when systems gain new capabilities, the conversation eventually shifts from can to should.

The Cashless Direction—and What Gets Lost

Digital payments are becoming the default. That’s driven by convenience, not coercion.

But as digital systems expand, physical alternatives tend to shrink.

Cash—and by extension, physical assets like gold and silver—offer properties that digital systems don’t:

- Direct ownership without intermediaries

- Privacy in ordinary transactions

- Resilience during outages or system disruptions

As those properties become less common in everyday finance, their value becomes more strategic.

Efficiency vs. Autonomy: The Tradeoff No One Emphasizes

FedNow and similar systems deliver undeniable benefits:

- Faster transactions

- Reduced settlement risk

- Greater operational efficiency

But every system optimizes for something—and often at the expense of something else.

In this case:

- Efficiency increases

- Centralization deepens

That doesn’t make the system inherently harmful. But it does mean users are more dependent on it.

And dependency changes the relationship between individuals and the financial system they operate within.

My Take: This Isn’t About Panic—It’s About Awareness

There’s a tendency to frame this conversation in extremes—either total trust or total distrust.

Reality is usually more nuanced.

FedNow is a tool. So is any future digital currency. The real question isn’t whether these systems exist—it’s how they evolve, and how much control they ultimately exert over everyday financial activity.

At the same time, dismissing physical assets as outdated misses the bigger picture. Gold and silver aren’t competing with digital systems—they’re hedging against them.

Different tools for different risks.

The Bottom Line

We’re moving into a financial environment where:

- Digital systems are faster and more integrated

- Monitoring capabilities are more advanced

- Physical alternatives are less emphasized

That doesn’t automatically lead to loss of freedom. But it does shift the landscape.

Understanding that shift—rather than ignoring it—is what allows people to make informed decisions about how they store, move, and protect their money.

Because in the end, the real divide isn’t digital vs. physical.

It’s control vs. independence.

And that’s a conversation worth paying attention to.

Final Word: Don’t Wait Until the System Changes Around You

If you’re seeing the direction this is heading, the worst move is doing nothing.

You don’t need to panic—but you do need to prepare.

The shift toward digital financial systems, FedNow-style infrastructure, and potential CBDCs isn’t theoretical anymore. It’s unfolding in real time. And once systems like programmable money are fully embedded, opting out becomes significantly harder.

That’s why getting informed now matters.

Download the Digital Dollar Reset Guide by Bill Brocius here

This isn’t casual reading—it’s a breakdown of what’s coming, how digital currency control could reshape financial freedom, and what steps you can take to stay ahead of it.

If you value financial autonomy, treat this like required intelligence—not optional information.