India’s Bold Move: Gold Repatriation Signals BRICS Challenge to US Dollar

Over 100 tonnes of gold have been moved from the United Kingdom to the Reserve Bank of India’s (RBI) vaults in one of the most ambitious transfers of the precious metal ever undertaken, and that amount could double in the coming months, according to a report from the Times of India published Friday.

Up until now, over half of the RBI’s gold reserves were being held with the Bank of England (BoE) and the Bank of International Settlements (BIS) overseas, but the Indian government has begun the process of repatriating the country’s bullion holdings.

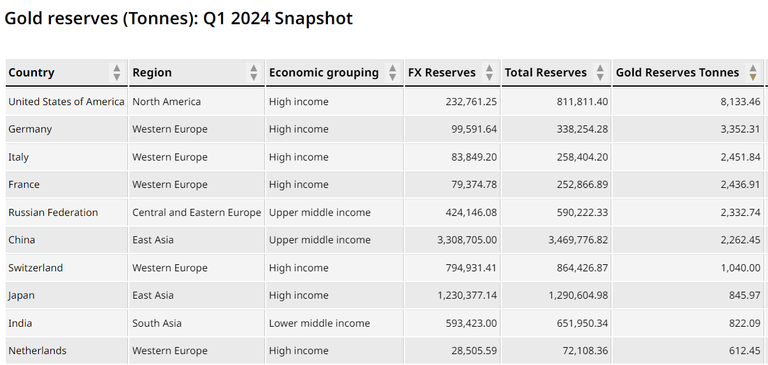

As of March 31, 2024, the RBI’s total gold reserves were listed at 822.1 tonnes, up from 794.63 tonnes in March of 2023, and 413.8 tonnes of that total was held overseas.

The Bank of England has long served as the storehouse for the bullion reserves of a large number of central banks, including those of India, with some of the country’s gold reserves housed in the UK since before Independence in 1947.

An unnamed Indian government official was quoted as saying that the decision was taken in part to cut back on the storage fees the RBI was paying to the BoE on the reserves, which have risen as the value of the bullion has appreciated to all-time high prices this year.

“RBI started purchasing gold a few years ago and decided to undertake a review of where it wants to store it, something that is done from time to time,” the official said. “Since stock was building up overseas, it was decided to get some of the gold to India.”

The secure movement of nearly $8.3 billion in heavy gold bars was a massive logistical undertaking, involving months of planning followed by careful execution with close coordination between the finance ministry, the RBI, and several other national and local government departments.

The RBI also needed to get a national customs duty exemption to ‘import’ the precious metal, as the bullion constituted a sovereign asset. There was no exemption from the goods and services tax on the gold, however, because this tax revenue is shared with the states.

The government also made use of specialized aircraft to transport the massive gold shipments, with the highest levels of security arrangements.

The 100 tonnes of gold has now joined the balance of India’s domestically-held gold reserves in the old RBI vaults on Mumbai’s Mint Road as well as the new state-of-the-art vaults located in the new RBI building in Nagpur.

“While no one was watching, RBI has shifted 100 tonnes of its gold reserves back to India from UK,” prominent economist Sanjeev Sanyal told India Today. “India will now hold most of its gold in its own vaults. We have come a long way since we had to ship out gold overnight in 1991 in the midst of a crisis.”

In 1991, Indian Prime Minister Chandra Shekhar was facing a severe balance of payments crisis after which it pledged to raise funds. Between July 4 and 18, 1991, the RBI was forced to sell 46.91 tonnes of gold to the Bank of England and the Bank of Japan, raising $400 million in the process.

Then, in 2009, India’s central bank purchased 200 tonnes of gold worth $6.7 billion from the International Monetary Fund (IMF) under Prime Minister Manmohan Singh.

According to the latest World Gold Council data, India’s sovereign gold reserves place it ninth in the world, just behind Japan, and the precious metal represents nearly 9% of its total foreign currency reserves, nearly double China’s 4.64%.

This article originally appeared on Kitco News