$130 Trillion Time Bomb: How Debt, FedNow, and CBDCs Are Quietly Reshaping Financial Control

The $130 Trillion Reality No One Wants to Deal With

Let’s strip away the spin.

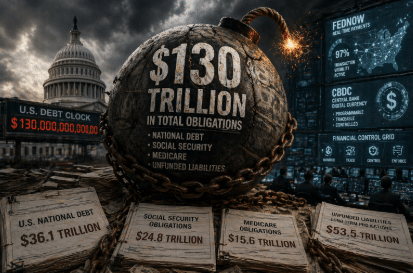

The U.S. isn’t just carrying national debt—it’s sitting on roughly $130 trillion in total obligations:

- Treasury debt already on the books

- Future Social Security payouts

- Medicare commitments

- Long-term liabilities buried in projections

This isn’t a short-term gap. It’s structural.

And when you’re dealing with numbers at that scale, the usual fixes don’t work anymore.

Why Traditional Solutions Break Down

You’ll hear the standard playbook:

- Raise taxes

- Cut spending

- Grow the economy

Sounds clean. Doesn’t hold up.

Raise taxes too much? You choke productivity.

Cut spending? Political gridlock shuts it down.

Rely on growth? The math doesn’t close fast enough.

So what’s left?

Not magic. Not miracles.

Control.

Not in the dramatic sense people imagine—but in the operational sense: tightening how money moves, where it goes, and how visible it is at every step.

When Debt Gets This Big, Visibility Becomes Mandatory

At $130 trillion, blind spots become liabilities.

A system under that kind of pressure needs:

- Accurate tracking of economic activity

- Reliable and enforceable tax collection

- Minimal “leakage” outside official channels

In plain terms: it needs to see everything.

That’s where the shift happens—from a loosely monitored financial system to one that prioritizes total visibility.

Not because it sounds good. Because the math demands it.

FedNow: Speed on the Surface, Visibility Underneath

FedNow is being marketed as a convenience upgrade.

Instant payments. Faster transfers. Modern infrastructure.

And yes—it does all that.

But look one layer deeper.

FedNow introduces:

- Real-time settlement

- Centralized transaction routing

- Immediate confirmation of fund movement

That means money no longer drifts through delays or blind spots. It moves instantly—and it’s visible instantly.

Once that framework exists, the system doesn’t just process payments.

It observes them. In real time.

From Infrastructure to Enforcement

Here’s where things evolve.

A system that can:

- See transactions instantly

- Route them centrally

- Record them permanently

Can also:

- Apply rules faster

- Enforce policies immediately

- Respond to behavior in real time

This isn’t theory. It’s capability.

And once capability exists, it tends to get used—especially under financial pressure.

CBDCs: Not Just Innovation—Policy Tools

Central Bank Digital Currencies (CBDCs) are often framed as upgrades:

- Faster payments

- Financial inclusion

- Technological modernization

But in a system carrying massive obligations, they serve another function.

They allow for:

- Programmable money (rules attached to spending)

- Direct transmission of policy (no intermediaries)

- Granular oversight of financial activity

That’s not just efficiency. That’s precision.

Why Control Starts Looking Like a Requirement

When obligations don’t shrink, priorities shift.

Suddenly:

- Tax compliance becomes non-negotiable

- Capital leaving the system becomes a threat

- Cash-based or informal economies become “problems”

From there, the incentives are clear:

- Reduce anonymous transactions

- Increase traceability

- Centralize how money flows

Again—this isn’t pitched as control.

It’s framed as stability.

The Narrative Flip Is Already Underway

Watch how the conversation changes.

It starts with:

“Let’s modernize payments.”

Then it becomes:

“We need better oversight.”

And eventually:

“Stability requires tighter systems.”

At that point, the question isn’t whether to increase control.

It’s how fast it can be implemented.

The Endgame: A Fully Integrated Financial System

A system carrying $130 trillion in obligations can’t tolerate:

- Opaque transactions

- Fragmented payment channels

- Limited oversight

It naturally moves toward:

- Integration across platforms

- Continuous visibility

- Enforceable financial rules

That’s the trajectory.

Not because of ideology—but because of pressure.

The Bottom Line

The $130 trillion figure isn’t just a headline.

It’s a constraint.

It limits how flexible the system can be.

It dictates how money must be tracked.

And it accelerates the adoption of tools that increase control over financial activity.

FedNow, digital payment rails, CBDC discussions—they’re not random developments.

They’re aligned responses to a system under strain.

What You Do With This Information Matters

You don’t need to panic—but you do need to pay attention.

Because once financial systems become:

- Fully digital

- Fully visible

- Fully enforceable

The room to operate outside those systems shrinks fast.

If you want a clear breakdown of where this is heading—and how to prepare—Download the Digital Dollar Reset Guide by Bill Brocius.

This isn’t optional reading if you’re thinking ahead. It connects the dots between rising debt, FedNow infrastructure, and the global push toward digital currency systems—and lays out practical steps to protect your financial autonomy.

You can ignore the signals.

Or you can recognize the pattern while there’s still time to adapt.