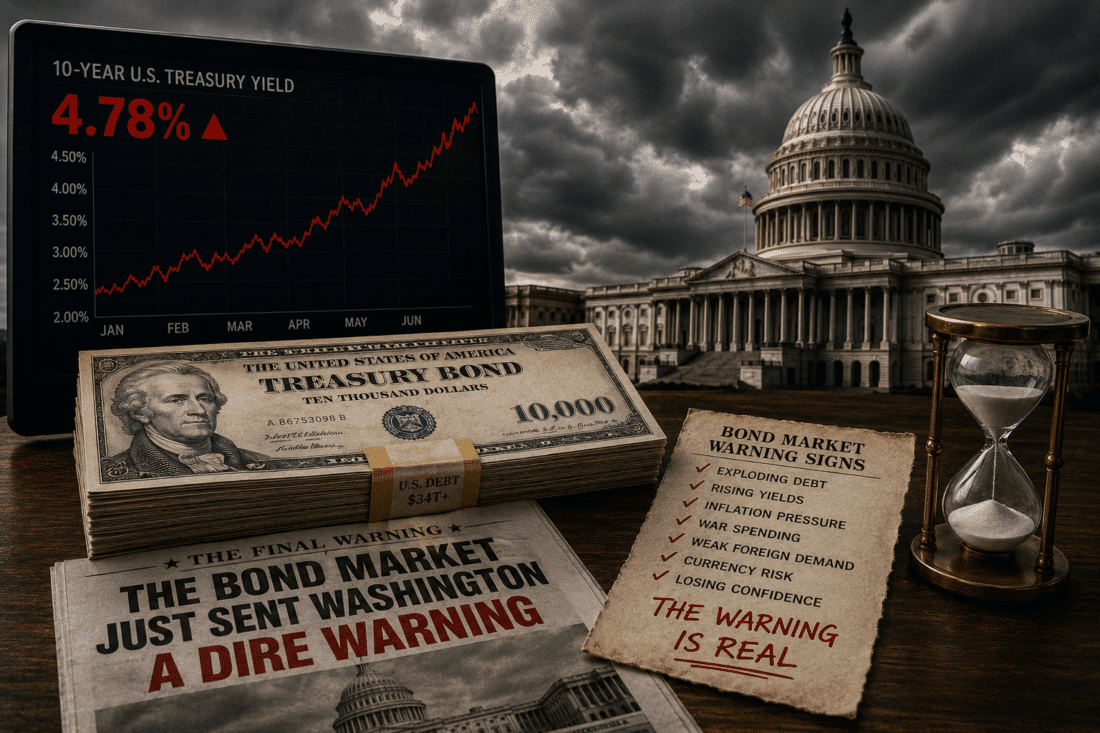

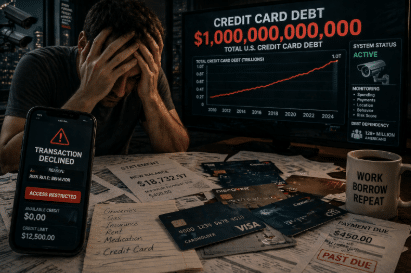

$1 Trillion in Credit Card Debt: The Quiet Expansion of Financial Surveillance and Programmable Money Control

The $1 Trillion Milestone Isn’t What You Think

They’re selling you a narrative about overspending.

“Consumers are stretched.”

“Inflation hit households hard.”

“People are relying more on credit.”

All technically true—and completely missing the point.

That $1 trillion in credit card debt isn’t just a sign of economic pressure. It’s proof that a massive portion of the population now depends on a fully digitized financial system to function day to day. Groceries, gas, emergencies—funded on revolving credit.

And here’s where it gets interesting: when your survival depends on credit, whoever controls that credit controls your options.

Your Credit Card Is Already a Surveillance Device

Forget the plastic. The real product isn’t the card—it’s the data.

Every transaction you make feeds a system:

- Where you spend

- What you buy

- When you buy it

- How often you deviate from patterns

This isn’t passive recordkeeping. It’s active monitoring.

Your financial behavior is being:

- Scored in real time

- Flagged for “risk”

- Used to adjust your access dynamically

If you think this is just about fraud prevention, you’re not looking deep enough. This is behavioral mapping at scale.

Debt Creates Leverage—And Leverage Gets Used

Here’s the part most people don’t want to confront:

Debt isn’t just a liability. It’s a control mechanism.

When millions of people are carrying balances:

- Credit limits can be tightened instantly

- Interest rates can shift without warning

- Transactions can be declined based on internal rules

You don’t need force when you have dependency.

And that dependency is now systemic.

People aren’t using credit as a backup anymore—it’s their primary financial buffer. That means any restriction, delay, or algorithmic decision hits immediately.

From Credit Scores to Behavioral Control

We’re already living inside a system that decides what you can and can’t do financially.

Right now, it looks like:

- Credit scores determining access

- Fraud systems blocking purchases

- Banks sending “unusual activity” alerts

But that’s just version one.

The next phase is obvious if you’re paying attention:

- Spending limits tied to behavior profiles

- Category-level restrictions (what you’re allowed to buy)

- Real-time approvals based on policy logic

Not someday. This is a natural extension of what’s already in place.

The infrastructure doesn’t need to be invented—it just needs to be expanded.

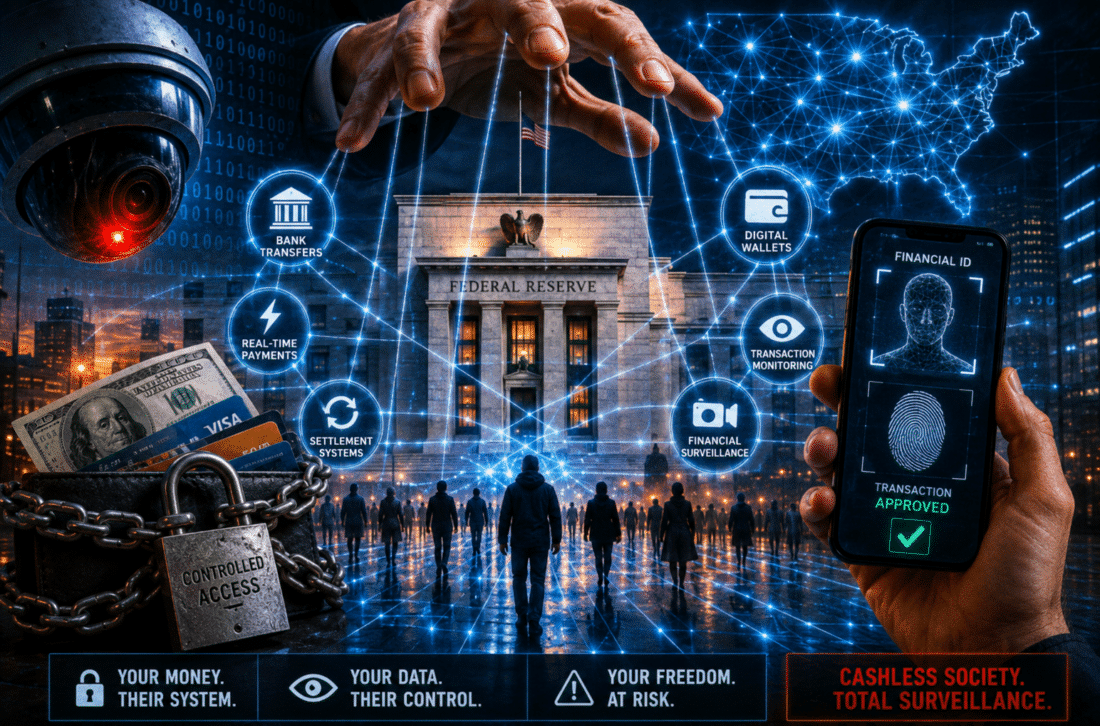

FedNow: The Rails for Instant Financial Control

Let’s talk about FedNow.

You’ll hear it described as a convenience upgrade—faster payments, instant settlement, modern banking. And sure, that’s part of it.

But speed isn’t the real story. Visibility is.

FedNow enables:

- Real-time transaction processing

- Immediate confirmation and settlement

- Centralized pathways for moving money

That means no delays, no buffers, no gaps.

In a system like that, control doesn’t just exist—it operates instantly.

And while FedNow itself isn’t a central bank digital currency (CBDC), it builds the exact infrastructure needed to support one. The rails are being laid before most people even realize where the track is going.

The Justification Playbook Is Already Written

Here’s how this always gets framed:

“Consumers are overleveraged.”

“Debt levels are a systemic risk.”

“We need better oversight to maintain stability.”

Sounds reasonable. That’s the point.

Because once you accept that premise, the next steps become easy to sell:

- Stricter lending controls

- Increased transaction monitoring

- Limits on “risky” spending behavior

It won’t be called control.

It’ll be called risk management.

A Highly Indebted Population Is Easier to Steer

This is the uncomfortable truth most analysts won’t say out loud:

When people rely on credit to survive, they become easier to guide.

Not through force—but through systems.

If your access to money can be:

- Adjusted

- Delayed

- Restricted

- Or revoked

Then your behavior can be influenced without ever issuing a command.

And when that system becomes fully digital—instant, programmable, and centralized—the level of precision goes way beyond anything we’ve seen before.

The Real Shift: From Financial Access to Financial Permission

We’re moving from a world where money is something you have…

to a world where money is something you’re allowed to use.

That’s the shift.

And once that line is crossed:

- Every transaction becomes conditional

- Every purchase becomes reviewable

- Every user becomes a data profile

This is where digital dollar systems, CBDC frameworks, and real-time payment networks all converge.

Not in theory—in function.

The Bottom Line

The $1 trillion credit card debt number isn’t just an economic warning.

It’s a structural one.

It tells you:

- People are dependent

- Systems are digitized

- Control mechanisms are already active

And as digital financial infrastructure expands, that control becomes faster, tighter, and harder to avoid.

What You Do Next Matters

If you’re seeing the pattern, then you already know this isn’t something to ignore.

Understanding where this is going—and how to position yourself outside the blast radius—is no longer optional.

Download the Digital Dollar Reset Guide by Bill Brocius

This isn’t casual reading. It’s a breakdown of how digital currencies, FedNow, and centralized financial systems are reshaping control—and what you can do to protect your financial autonomy before those systems fully lock in.

You can wait until it’s obvious.

Or you can get ahead of it while there’s still room to move.