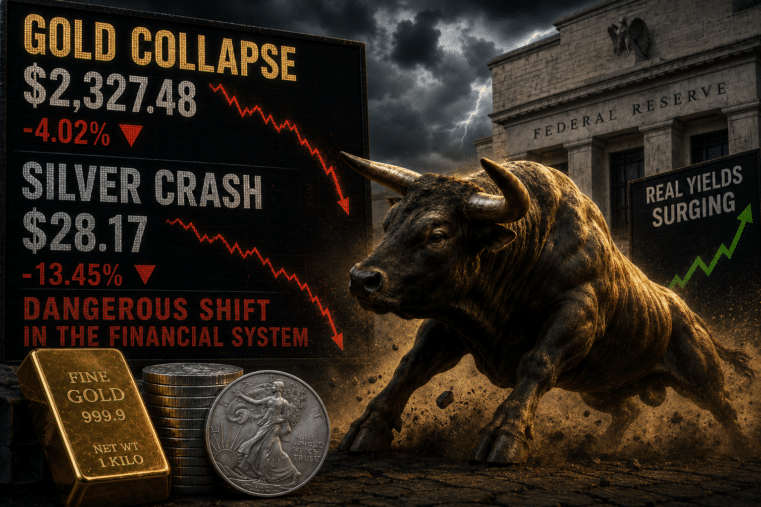

GOLD’S “FAKE FLOOR” WARNING: Why the Smart Money Is Preparing for More Turbulence — And Why That’s Not Bearish

Heraeus Says “More Downside Ahead.” Are They Wrong?

Let’s start here: I don’t think Heraeus is crazy.

When you see silver run 70% in a month and hundreds of percent over a year, history tells us something important — markets don’t move in straight lines forever. After the spikes in 1980 and 2011, we saw deep corrections. Anyone who’s been in this market long enough remembers the pain that followed those blow-off tops.

So yes, we could see more downside before a real floor forms. That’s not fearmongering — that’s market structure.

Silver is volatile. It overshoots both directions. It’s like that old muscle car I drove in my twenties — powerful, exciting, but you better keep both hands on the wheel.

But here’s where the conversation gets more interesting.

This Is Not 1980. This Is Not 2011.

Back then, we didn’t have:

- Trillion-dollar annual deficits as the norm

- Central banks accumulating gold at record levels

- Open geopolitical escalation in multiple regions

- Ongoing trade instability and tariff uncertainty

- A global public increasingly skeptical of fiat currency systems

Those are structural shifts, not short-term headlines.

When analysts compare today’s rally to past spikes, they’re focusing on price behavior. I’m focused on monetary conditions.

And those conditions are unlike anything I’ve seen in my four decades in finance.

Volatility Doesn’t Equal Weakness

Let’s be clear: a 20%–30% pullback in silver would not shock me.

But here’s the key distinction — is it a collapse in fundamentals, or is it a reset in sentiment?

There’s a difference.

The article correctly notes that excessive optimism needs to be worked off. Markets need to cool down. That’s healthy. What’s not healthy is ignoring why capital is flowing into precious metals in the first place.

Gold didn’t rally because people got bored.

It rallied because confidence in systems is fraying.

Geopolitical risk boosted gold. Trade uncertainty boosted gold. Fiscal instability boosted gold. And central bank accumulation continues to provide a long-term foundation.

Short-term price swings don’t erase long-term monetary stress.

The “Wait for the Perfect Bottom” Trap

This is where everyday investors get hurt.

I’ve watched people try to time gold for 40 years. They wait for the perfect dip. Then it moves higher. Then they wait again. Then they buy emotionally after a surge.

Gold and silver aren’t day-trading vehicles for most people reading this.

They’re insurance.

You don’t wait for your house to catch fire before you buy coverage.

If prices soften, disciplined buyers accumulate methodically. If prices rise, disciplined buyers hold patiently. The strategy doesn’t change because the ticker wiggles.

Why This Moment Is Different for Everyday Investors

My readers aren’t hedge funds. They’re retirees, small business owners, working families trying to protect purchasing power.

They feel:

- Higher grocery bills

- Insurance premiums climbing

- Housing costs rising

- Savings earning less in real terms

The question isn’t “Will silver retrace 25%?”

The real question is:

Is the purchasing power of fiat currencies becoming more stable — or less?

Every major fiscal and geopolitical signal says less.

That’s why central banks aren’t selling gold. They’re buying it.

And they’re not doing it for a short-term trade.

What I’m Watching Closely

Here’s what actually matters going forward:

- Central bank demand – Still historically strong.

- Debt expansion – Governments continue spending aggressively.

- Global instability – Conflicts and trade uncertainty remain unresolved.

- Investor psychology – Excess optimism may fade, but underlying demand hasn’t disappeared.

If sentiment resets while structural drivers remain intact, that’s not bearish long-term.

That’s transitional.

The Bigger Picture Most Analysts Miss

Markets are not just technical charts. They’re reflections of trust.

Trust in governments.

Trust in currencies.

Trust in institutions.

When trust weakens, hard assets strengthen.

Even if we see additional price declines in the short term, the macro forces pushing gold and silver into the spotlight haven’t reversed.

They’ve intensified.

So Do I Agree With the Takeaway?

Partially.

Yes, we could see lower prices before a definitive floor.

No, that does not weaken the long-term case for holding precious metals as financial protection.

In fact, periods of volatility often separate speculators from strategic investors.

And I know which group I’d rather stand with.

Final Thoughts

If you’ve been feeling uneasy watching the price swings — that’s normal.

Volatility shakes confidence. Headlines amplify fear. Analysts debate floors and retracements.

But beneath the noise, one thing hasn’t changed:

The global financial system remains heavily leveraged, politically strained, and structurally fragile.

Gold and silver don’t need perfect charts to justify their role.

They need imperfect systems.

And we have plenty of those.

If You Want the Real Strategy Behind the Headlines…

There’s a difference between reading market commentary and understanding how to position yourself intelligently within it.

That’s exactly what we focus on inside Inner Circle — cutting through short-term noise, identifying structural trends, and protecting wealth with discipline instead of emotion.

If you want deeper analysis, portfolio positioning insights, and ongoing guidance during this volatile cycle, I invite you to join us.

Join Inner Circle today and stay ahead of the next move — instead of reacting to it.