Gold’s Resurgence: Is the Bull Run Just Beginning?

With athletes around the world preparing for this summer's Olympic games in Paris, one analyst likened the yellow metal's recent rally to a sprint against the best runners in the world, with the lustrous metal “heading for gold.”

According to Nitesh Shah, Head of Commodities and Macroeconomic Research at WisdomTree Europe, “Exchange-traded product (ETP) investors who had sat on the sidelines for some time are now starting to cheer the metal on in some corners of the world,” and the primary hope is that “the metal doesn’t run out of energy too soon.”

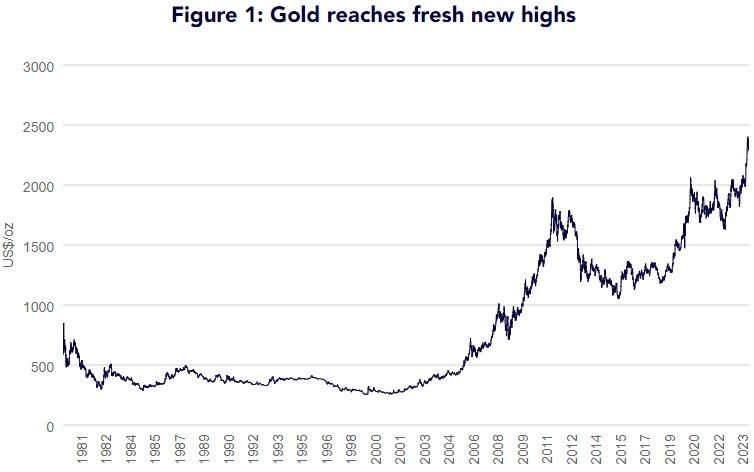

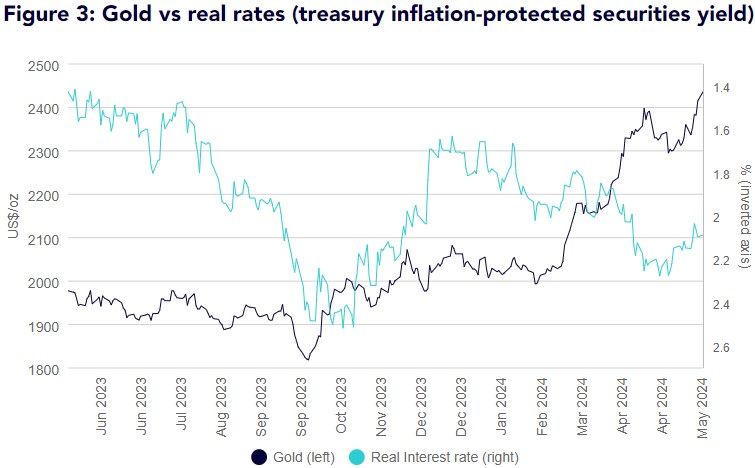

“Gold hit a fresh high once again on 17 May 2024 at US$2402.60/oz1,” Shah said. “Since its previous high on 12 April 2024 (at US$2401.5/oz), gold eased for most of the month on expectations of ‘higher for longer’ interest rate expectations in the US. The March US consumer price index [CPI] inflation, which was printed in April, was a catalyst for gold strength despite the elevated bond yields and strong dollar headwinds.”

While the March CPI provided a boost to gold, April’s CPI print didn’t have the same effect, he noted, as “it missed market expectations.”

“However, a growing sense that it affords the US Federal Reserve (the Fed) to cut rates earlier has helped the metal move to a fresh high,” Shah said. “Indeed, retail sales and industrial production data misses in April have also given the market more hope that one to two rate cuts will indeed be delivered this year (even if not the six the market was expecting at the beginning of the year).”

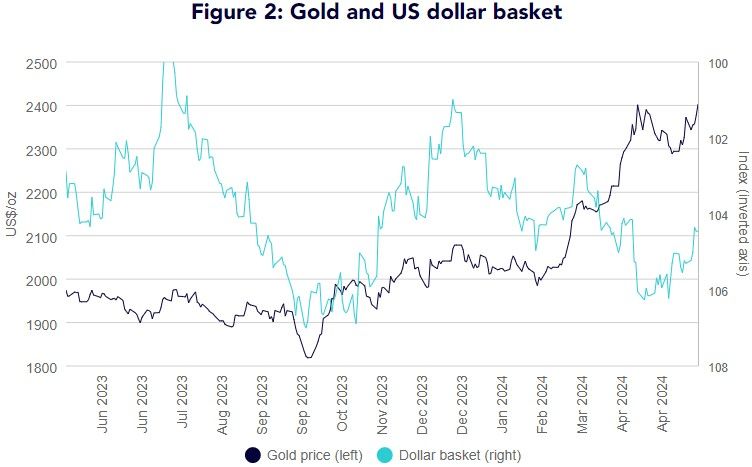

A dip in the U.S. dollar has also benefited gold over the past three weeks, he noted.

And a drop in bond yields during that period has also been a boon for the precious metal.

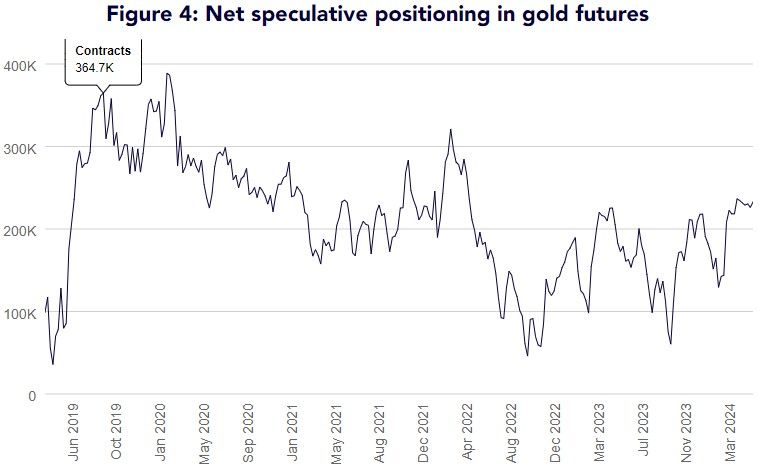

“Sentiment towards gold remains strong, with net speculative positioning hovering at the 230k handle since mid-April 2024,” Shah said.

He highlighted investment demand for physical gold in China as the primary source of strength for the precious metal over the past month.

“Chinese gold ETPs have seen inflows five months in a row,” Shah noted. “April attracted RMB9bn (US$1.3bn), the strongest month on record, pushing the total assets under management (AUM) to another historical high of RMB46bn (US$6.4bn). Meanwhile, holdings also registered the largest ever monthly increase, rising 17t to 84t.”

The one industry that has seen a cool-down in demand is the jewelry sector, which Shah attributed to the rapid rise in gold prices.

“April is normally a period for retailers to restock ahead of the May Day Holiday (1-5 May),” he said. “However, this year, retailers approached the period with caution given the higher prices and consumer price sensitivity. Indeed, Shanghai premiums over London prices have eased, indicating less willingness to pay over the odds for the metal.”

It was a similar story in India, which saw a 50% year-over-year (y/y) reduction in demand in March amid rising prices.

“Indian gold bullion imports more than halved y/y to 30t in March due to higher prices and weak consumer demand,” Shah said. “Following the recent price pull-back, there has been a slight improvement in physical demand. However, volumes have remained weaker than in a normal period of weddings and ahead of Akshaya Tritiya (an extremely auspicious day to buy gold, which fell on 10 May this year).”

Global ETP flows remain the primary outlier as they “have been negative over the past year, indicating that many institutional investors do not share the same level of enthusiasm for the metal as the retail market,” Shah said.

“However, Chinese investors have bucked this trend,” he concluded. “In recent weeks, we have witnessed some strong flows into US-domiciled ETPs as well, possibly pointing to outflows reaching a base.”

This article originally appeared on Kitco News