SHOCK VOTE: Senate Slams the Brakes on the Digital Dollar—FedNow, CBDC Agenda EXPOSED as Stablecoins Rise to Power

The Headlines Say “Victory”—But Look Closer

The headlines are already spinning this as a victory: no official digital dollar, no immediate rollout of a central bank digital currency, no direct Federal Reserve control over programmable money—at least not yet. But if you think the machine just backed off, you’re missing how this game is played. Power doesn’t disappear, it reroutes. And what’s quietly stepping into the gap is something most people are celebrating without understanding—private stablecoins.

Stablecoins Are Not an Alternative—They’re the Next Phase

USDT, USDC, and the next wave already forming behind them aren’t just alternatives to a CBDC, they’re the testing ground. The Senate may have slowed down a government-issued digital dollar, but it effectively opened the floodgates for corporations to issue their own versions of money. That means Americans are being handed “choice,” but it’s a curated kind of choice—one where every option still plugs into a rapidly expanding system of digital financial control.

The Illusion of Choice in a Controlled System

On the surface, it sounds like freedom. You get to choose your stablecoin. You get competition. You get innovation. But zoom out for a second. When corporations issue the currency, they control the environment it operates in. That means terms of service replace law, algorithms replace discretion, and access can be modified, restricted, or revoked at any time. This is what programmable money really means—not just digital dollars, but digital rules attached to every transaction.

Corporate Currencies and the Fragmentation of Control

Now picture where this is heading. Amazon launches its own stablecoin, offering discounts and incentives to keep spending locked inside its ecosystem. Google ties a digital currency into identity, data tracking, and advertising infrastructure. Apple embeds payments directly into hardware, biometrics, and closed software loops. What you end up with isn’t just convenience—it’s a network of corporate-controlled micro economies where your money only works the way they decide it should. That’s not decentralization. That’s fragmentation of control across powerful entities that all play by the same surveillance-friendly framework.

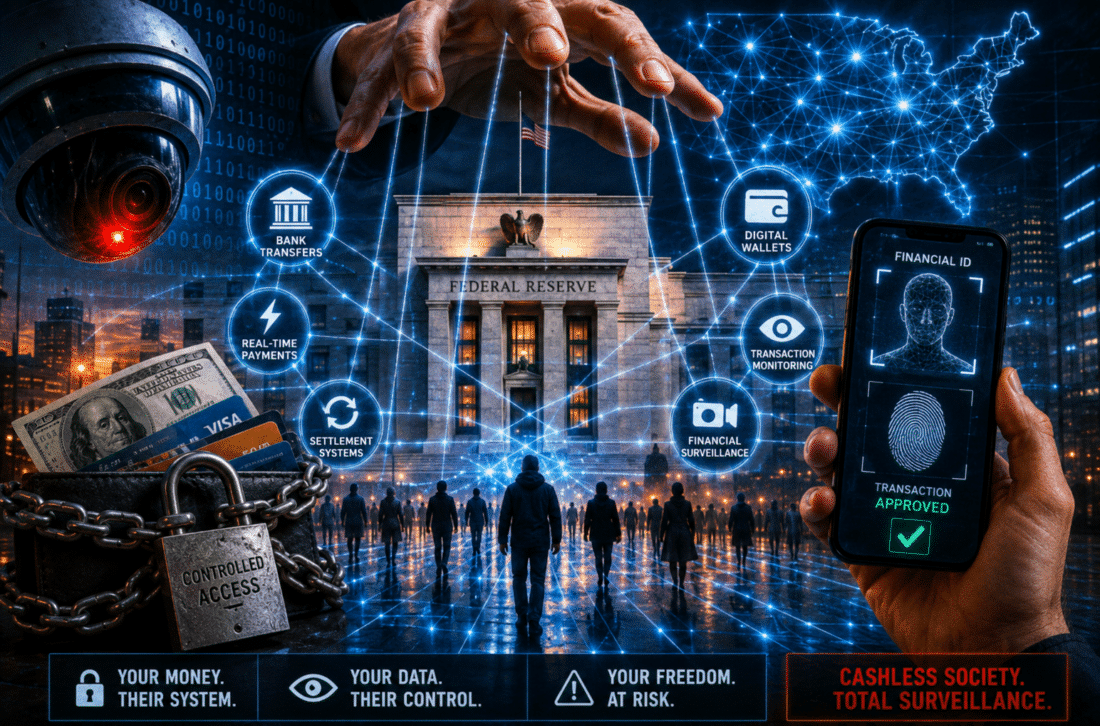

FedNow: The Quiet Backbone of the New Financial System

And behind it all sits the real infrastructure nobody is talking about enough—FedNow. While the public debate fixates on CBDC versus stablecoins, FedNow is already operational, enabling instant, 24/7 payments across the U.S. banking system. It’s the rail system for the next era of money. Whether it’s a government-issued digital dollar or a corporate stablecoin, they all run smoother, faster, and with more visibility because of systems like this. You don’t need a CBDC to build financial surveillance when the transaction layer is already in place.

The Incentive Structure Most People Miss

To understand where this goes, you have to follow the incentives. Take USDT as an example. It’s backed largely by cash equivalents, with a heavy allocation to U.S. Treasury bills. That means the issuer can generate yield—3, 4, even 5 percent—on billions of dollars while users treat the token like a simple digital dollar. It’s a quiet but powerful model: issue digital currency, park the reserves in yield-generating instruments, and collect the spread. Now scale that model across Big Tech, major retailers, and financial institutions. You’re not just looking at competition with banks—you’re watching the emergence of an entirely new monetary layer built on top of the old one.

Programmability Means Control—No Matter Who Issues It

But here’s where it gets more serious. The same mechanisms that make stablecoins efficient also make them controllable. Transactions can be monitored in real time. Funds can be frozen. Spending categories can be restricted. Access can be tied to identity, compliance, or behavior. This isn’t speculation—it’s how programmable financial systems are designed. Whether those controls come from governments, corporations, or a combination of both is almost beside the point. The capability exists, and once it’s normalized, it rarely gets rolled back.

This Isn’t a Stop—It’s a Strategic Delay

So what does this Senate decision really represent? Not a defeat of the digital dollar agenda, but a delay—a strategic pause that allows the private sector to normalize digital currencies while the infrastructure matures. By the time a central bank digital currency re-enters the conversation, people will already be used to living inside a cashless, trackable, programmable financial system. At that point, resistance becomes a lot harder, because the convenience will already be baked into daily life.

The Shift Most People Won’t See Until It’s Too Late

This is the monetary shift most people won’t recognize until it’s fully locked in. Cash fades out. Digital systems take over. Control moves from physical possession to network permission. And the illusion of choice keeps people from questioning the structure being built around them.

What This Means for You Right Now

If you’re paying attention, you know this isn’t something to brush off. Understanding how the digital dollar, FedNow, stablecoins, and CBDC systems intersect isn’t just interesting—it’s critical. The rules of money are changing in real time, and the people who don’t adapt are the ones who get caught inside systems they don’t control.

Don’t Wait Until You’re Locked In

If you want a clear breakdown of what’s coming and how to protect your financial autonomy before programmable money becomes the default, you need to get ahead of it now. Download the Digital Dollar Reset Guide.

Because by the time this system is fully operational, opting out won’t feel like a choice—it’ll feel like a memory.